Currencies

The £ has been relatively range bound this week, with continued tightening of Covid measures and various local lockdowns now in place. There have also been added complications from Boris Johnson’s announcement warning businesses to prepare for a no deal Brexit, commenting that there has been ‘little progress coming from Brussels’.

Looking at the US, the election is little more than a week away and Trump is still struggling to achieve any sort of Covid fiscal package passed through the House of Representatives. In Europe there has been some good news with the latest construction data looking better than expected but Brexit uncertainty has put a cap on any rally.

Wheat

Wheat markets have continued to strengthen during the week, supported by the dryness in South America and Russia. There continues to be strong demand from China for US material, and fund holders are now holding historic long positions. The French Matiff futures exchange is finding support from the reduced maize tonnage which is now beginning to impact UK prices. The prices of UK imports are now at a premium to domestic prices (reversing the situation from less than two months ago), and millers are beginning to lower their protein spec requirements, which means that some of the low grade milling wheat which was destined for feed wheat, is now finding a premium home again – which will tighten our market further. This development suggests that until such times as the European market breaks, there is no real reason for UK prices to come cheaper.

On a more positive note, UK plantings for harvest 2021 have continued at a good pace this week, but with prices at a £26 discount for new crop and concerns over dryness elsewhere, could it be that this is the level at which prices will stay? The crop emergence over the next few weeks and months will be critical for giving the market direction.

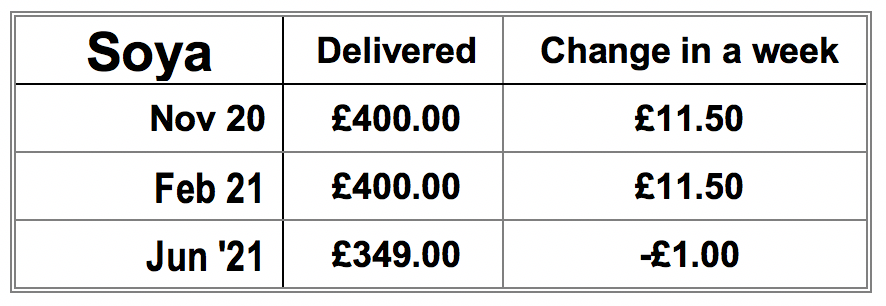

Soya

Soya prices have continued to rally with the US harvest now 80% complete. The global soya meal trade year on year stands at 67.8 MlnT, compared to 66.2 MlnT last year with the market taking that increased demand as being bound for the Chinese. South America continues to look dry with their La Niña weather pattern.

Brazil has had to replant some of their acreage meaning that they are now experiencing their slowest planting pace in 10 years. This will also put pressure on US beans as Brazilian beans are usually available January time and this replanting will delay them until February/March time. Low water levels in Argentina are causing issues for crushing facilities and needs to be kept an eye on.

And Finally…

Cow Cuddling trend sees people flock to farms in a bid to ease their stress and anxiety.

A growing wellness trend in the Netherlands has seen people spending many hours cow cuddling. The trend called ‘koe knuffelen’ relies on the animals warm temperature and size to boost oxytocin levels which can help reduce stress.

There are now several farms across the country offering the therapy and the demand has been huge, especially given the struggles 2020 has bought.

This follows on from Goat Yoga which was introduced a few years ago by a lady in America who believed getting the animals involved gave her clients a sense of ‘getting back to nature.’ Since then the trend has taken off globally to include pigs and even lemurs!

Regards,

Kay Johnson & Martin Humphrey