Currencies

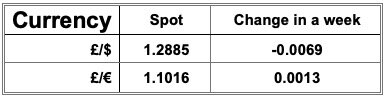

The £ did briefly creep back above 1.30 against the $ this week with the US continuing to struggle passing any form of fiscal relief package, however, it fell back below that level towards the later part of the week as investors become concerned about the continuing rising level of Covid cases and looked for traditional ‘safe’ investment markets.

Against the €, movement has been negligible with Brexit talks continuing yet no real fresh news to give direction.

Brexit and the evolving ‘three tier’ lock down measures in the UK will continue to be the main drivers and will continue to make for volatile markets.

Wheat

Wheat markets have seen yet another choppy week. The USDA report last week which lowered US production and the carryout was initially seen as bullish and rallied markets to two year highs, with the Matiff and Liffe futures exchanges following. US funds bought an additional 15,000 contracts meaning they were at close to historic highs of being long (bought in anticipation of further rises) of a total of 200,000 contracts. The sentiment then changed to take into account the fact that global carryout was upgraded, mostly down to Russia, up to 317 MlnT and prices eased.

Towards the end of the week there were concerns about dryness in South America and Russia, and prices then crept back up. In the UK we are still in an inverse market with demand for nearby physical product being strong, meaning that physical premiums are now moving above futures. The planting story is what is keeping UK prices supported and as we approach the end of the year, and begin to receive planting data from the AHDB (amongst others), the belief is that prices will break.

There has been a strong amount of sellers looking to make sales forward into next harvest but buyers are thin on the ground with consumers using hand to mouth.

Soya

Soya prices have also continued their upward trend this week following the report on Friday which put US old crop carryout at its lowest in 4 years, coupled with news that Brazilian beans will not be available until February now.

Global stocks dropped by around 5 MlnT and global demand was increased by 1.5 MlnT year on year, with 1 MlnT of that coming just from China. China are now back from their public holiday and continue to be strong buyers.

The South American 20/21 crop is estimated to be around 133 MlnT, which would be a record crop, however, like wheat, continued dryness across the country is meaning that this figure may well be downgraded. South American farm sales are still very slow with premiums rising $15 this week, but that doesn’t seem to be enough to encourage sales. New crop sales are currently half of what the normal levels

And Finally…

Charity ‘Free Cakes For Kids’ sees a huge rise in demand during 2020.

For children the idea of a birthday cake with candles is a given, but for children whose families are in financially difficult times due to lack of funds, health issues, or temporary living conditions, this is simply not possible.

That’s why the charity, ‘Free Cakes For Kids’ was first set up with a small team of volunteers in Oxford. There are now 60 groups across the country busy baking!

2020 has seen a huge demand for their services which tends to come via other services such as local food banks or womens’ refuges. One mum who was living with her three year old in a refuge told how the charity created a bespoke pirate themed cake for her sons birthday which meant that all the children living there could attend a birthday party. It gave them all something ‘normal’ in a very unsettling period of their lives.

Regards,

Kay Johnson & Martin Humphrey