Currencies

The £ is back to being `range bound’ against both the $ and the €. There has been little news from the Brexit discussions this week and in terms of the UK economy, there has been nothing there to offer any real support with greater restrictions continuing to be implemented across certain parts of the country.

The £ did see some benefit from the weakening $ earlier in the week following Trump’s diagnosis, and the continued issues with passing any sort of Covid stimulus package

Wheat

Wheat markets have continued to rally following the shock statistics revisions by the USDA last week.

The cut to the figures, coupled with concerns about dryness across certain parts of the US, Russia and Argentina meant that funds in the US bought heavily and extended their already long positions to around 200,000 contracts.

The Matiff and Liffe wheat markets ultimately followed with UK prices finding further support from confirmations by the Minister for Agriculture that this years wheat crop was 10.133 MlnT, 37% down on last year and the smallest crop since 1981.

Friday’s WASDE report has now revised global end stocks for 20/21 upwards on the back of Russia’s large crop but this will take time to filter through. There is still real demand in the UK for front end months which is beginning to push November physical premiums above futures. The discount between old and new crop now stands at around £25/T and how plantings are progressing globally over the coming weeks, will dictate if that discounts widens further. or narrow. Wheat prices will feel pressure the further into the corn harvest we progress, as this will ease the demand currently being felt on the spot market.

The UK still has a huge barley surplus with limited export interest which will also feature heavily through the rest of this season now at circa £45 discount to wheat.

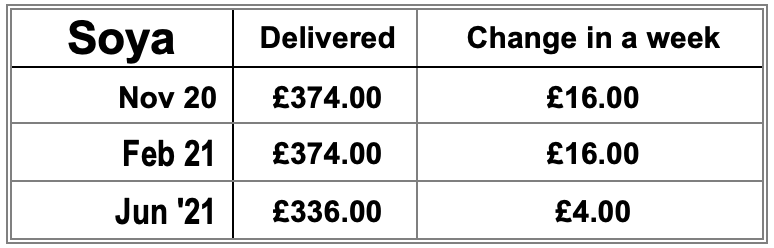

Soya

Soya followed the same pattern as wheat. With the USDA tightening figures and Chinese demand still strong, despite their public holiday, soya prices have rallied.

The USDA also reported their second biggest ever summer drawdown of stocks in September, 858 billion bushels. This drove funds to again increase their long position by a further 20,000 contracts. Friday’s WASDE report reduced the 20/21 crop carryout by 4.9 MlnT.

Brazilian plantings have been slow, so harvest will be delayed, with little availability until February (relatively late compared to other years), adding pressure to US stocks.

There have been more sales of Argentinian soya to China this week showing that the 3% reduction in export tax by the government to help drive farm sales is beginning to work

And Finally…

Rare 2,000 year old Roman coin commemorating the assassination of Julius Caesar is expected to fetch £5 million at auction.

The coin, which is over 2 millennia old, and one of only three to be known in existence, had been minted with the words ‘naked and shameless’ in celebration of the statesman’s death.

Caesar was murdered by a conspiracy of around 60 Roman senators in 44 BC who feared that his dictator style leading would allow him to name himself as King. Caesar had proved popular with the lower and middle classes and his assassination ultimately caused the fall of the republic.

If the coin reaches its estimate, then it would become the most expensive Roman coin to have ever been sold.

Regards,

Kay Johnson & Martin Humphrey