Wheat

Grain markets have been fairly flat over the past month. With London November futures moving off the board the market is now pricing off the May24 period. May futures ranged from £195 to £203 over the course of the month and prices are tending to bounce within this range depending on the news story of the day.

Current stories that continue to dominate the market are:

• Ukraine export corridor continues to function well as present, whether that be through the black sea corridor or via the Danube and up through EU.

• Increase buying demand from China.

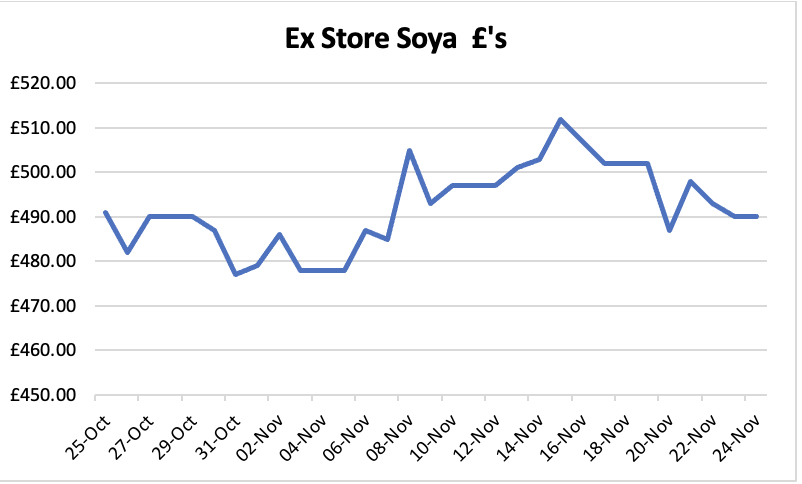

Soya

Soya has another volatile month with some sharp movements from day to day and generally trading within a £30 market range. Despite this today’s levels are almost unchanged versus this time last month.

The market is very much driven by the South American weather situation and prices will change wildly depending on updated weather forecasts. After poor planting conditions in both Brazil and Argentina it now looks like harvest in those countries will be delayed which will cause world supply issue come next March as the US stocks will be down to bare minimum and in need of the SA crop to supplement the market.

Sterling is performing better versus both the Dollar and Euro following recent inflation news and the autumn budget. This will help with the price of soya and other imported material. Currently sterling is £1.26 versus the dollar, it is worth remembering if that level falls back to £1.23 as it has been in recent months then we would need to add another £10 onto todays levels.

Organic

The organic market is tending to mirror that of the conventional market with cereals and soya both unchanged. Demand remains steady to subdued, with buying interest on the straights tending to be hand to mouth whereas in previous years compounders would look to forward cover.